Canada Tax Brackets 2025: See New Rates & Save

Big news for Canadian taxpayers! The federal government has implemented a significant middle-class tax cut that took effect on July 1, 2025, reducing the lowest tax bracket from 15% to 14.5% for 2025 (and 14% for 2026 and beyond). This change, combined with updated tax brackets adjusted for inflation, means nearly 22 million Canadians will save money on their taxes this year.

Whether you’re filing taxes for the first time or looking to optimize your tax strategy, this comprehensive guide covers everything you need to know about Canada’s 2025 tax brackets, new rates, and proven strategies to keep more money in your pocket.

What’s New in 2025: Key Changes at a Glance

Federal Tax Rate Reduction

- Lowest tax bracket reduced from 15% to 14.5% for 2025

- Further reduction to 14% starting in 2026

- Maximum annual savings: $574 for individuals, $840 for couples

- Who benefits: All taxpayers, with lower-income earners seeing the biggest percentage savings

Updated Tax Brackets

- All federal tax brackets indexed to inflation by 2.7%

- Basic personal amount increased to $16,129 (up from $15,705)

- RRSP contribution limit raised to $32,490 (up from $31,560)

- TFSA contribution limit remains at $7,000 annually

Understanding Canada’s Progressive Tax System

Canada uses a progressive tax system, meaning you pay different rates on different portions of your income. Think of it like climbing stairs – each step up represents a higher tax rate, but you only pay that higher rate on income above each threshold.

How It Works

- Federal taxes are the same across Canada

- Provincial taxes vary by province/territory

- Your total tax = Federal tax + Provincial tax

- Tax brackets apply to taxable income (after deductions)

2025 Federal Tax Brackets Breakdown

Here are the updated federal tax brackets for 2025, reflecting both the inflation adjustment and the new middle-class tax cut:

| Income Range | Tax Rate | What This Means |

|---|---|---|

| Up to $57,375 | 14.5% | Reduced from 15% – everyone benefits! |

| $57,376 – $114,750 | 20.5% | Only income in this range taxed at 20.5% |

| $114,751 – $177,882 | 26% | Only income in this range taxed at 26% |

| $177,883 – $253,414 | 29% | Only income in this range taxed at 29% |

| $253,415 and over | 33% | Highest earners pay 33% on income above this threshold |

Canada’s 2025 Federal Tax Brackets showing progressive tax rates from 14.5% to 33%

Real-World Example

If you earn $80,000 in 2025:

- First $57,375 taxed at 14.5% = $8,319

- Remaining $22,625 taxed at 20.5% = $4,638

- Total federal tax: $12,957

Provincial Tax Considerations

Your provincial tax depends on where you live on December 31st of the tax year. Each province has its own tax brackets and rates that apply in addition to federal taxes.

Top Combined Tax Rates by Province (2025)

| Province | Combined Top Rate | Best for High Earners? |

|---|---|---|

| Ontario | 53.53% | Lower rates available |

| British Columbia | 53.50% | Competitive middle brackets |

| Quebec | 53.31% | Higher rates but more services |

| Manitoba | 50.40% | Moderate rates |

| Alberta | 48.00% | Lowest combined rate |

| Saskatchewan | 47.50% | Most tax-friendly |

Top combined federal and provincial marginal tax rates across Canadian provinces for 2025

Pro Tip: If you’re planning to move provinces, consider the timing. Your provincial tax is based on where you live on December 31st, so a strategic move could affect your tax bill.

Smart Tax-Saving Strategies for 2025

1. Maximize Your RRSP Contributions

The #1 tax-saving strategy for most Canadians is maximizing RRSP contributions:

- 2025 limit: $32,490 or 18% of 2024 earned income (whichever is lower)

- Tax savings: Immediate deduction at your marginal tax rate

- Deadline: March 3, 2025 for 2024 tax year deduction

- Carry-forward: Unused room carries forward indefinitely

Example: If you’re in the 30% tax bracket and contribute $10,000 to your RRSP, you’ll save $3,000 in taxes immediately.

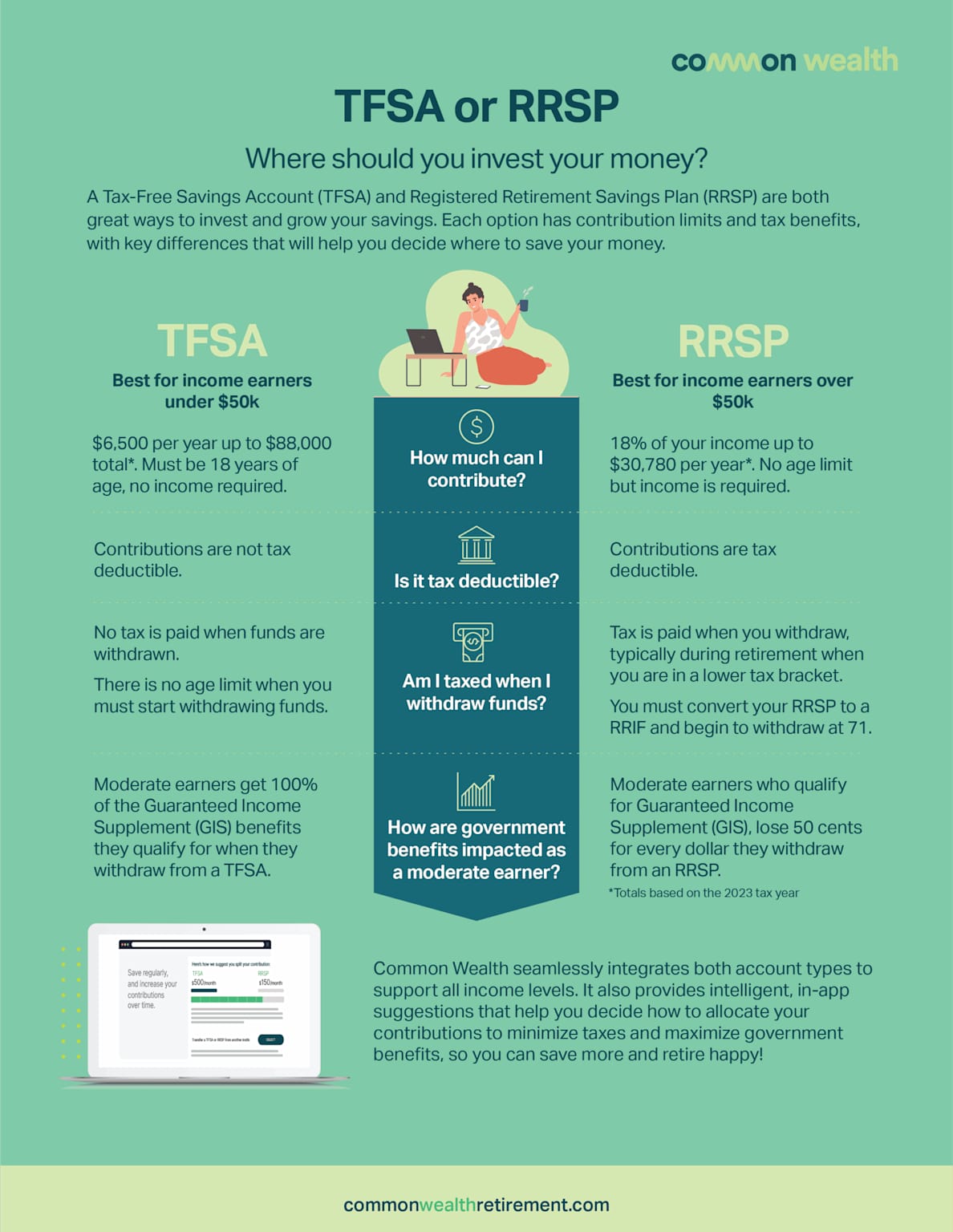

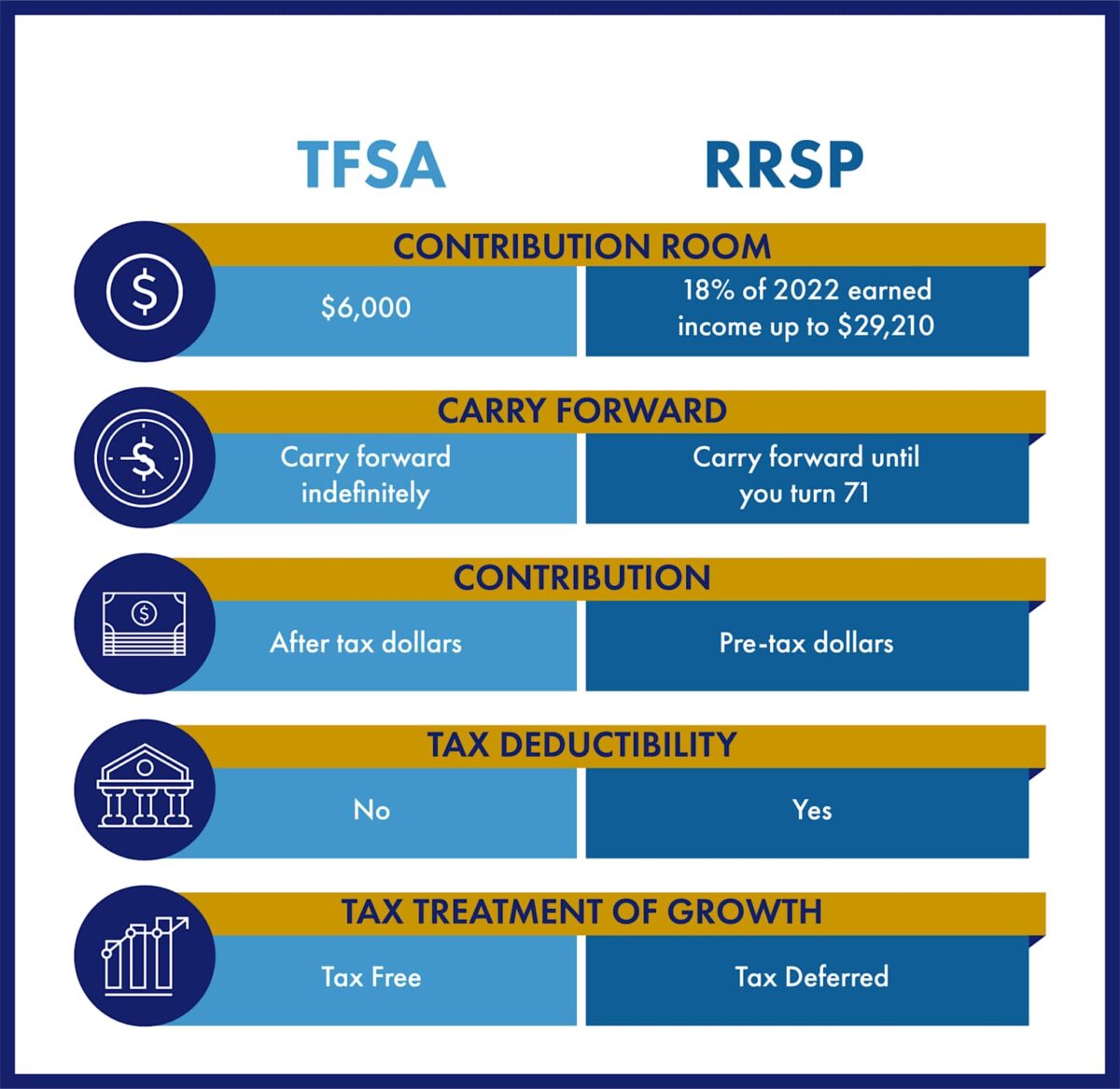

2. Use Your TFSA Room Strategically

Tax-Free Savings Accounts offer tax-free growth and tax-free withdrawals:

- 2025 limit: $7,000

- Lifetime contribution room: $102,000 (if eligible since 2009)

- Best for: Emergency funds, short-term goals, or supplementing retirement savings

- Flexibility: Withdraw anytime without penalty

Comparison of TFSA and RRSP accounts highlighting contribution limits, tax treatment, and impact on government benefits for Canadian savers

3. Claim All Available Tax Credits

Don’t miss these valuable credits:

- Basic Personal Amount: $16,129 (everyone gets this)

- Medical Expenses: Claim amounts over $2,834 or 3% of net income

- Charitable Donations: 14.5% credit on first $200, then 29% or 33%

- Tuition Fees: 14.5% credit, unused amounts carry forward

- Home Office Expenses: If you work from home

RRSP vs TFSA: Which Should You Choose?

The eternal Canadian question! Here’s a simplified decision framework:

Choose RRSP If:

- You’re in a high tax bracket now (over $50,000)

- You expect to be in a lower tax bracket in retirement

- You want an immediate tax deduction

- You’re focused on retirement savings

Choose TFSA If:

- You’re in a low tax bracket now (under $50,000)

- You expect to be in a higher tax bracket later

- You want flexibility to withdraw funds

- You’re saving for non-retirement goals

Comparison of TFSA and RRSP accounts in Canada highlighting contribution limits, tax treatment, and carry forward rules

The Smart Strategy: Use Both!

Many financial experts recommend using both accounts:

- Max out RRSP for immediate tax savings

- Use TFSA for tax-free growth

- Prioritize based on your current tax bracket

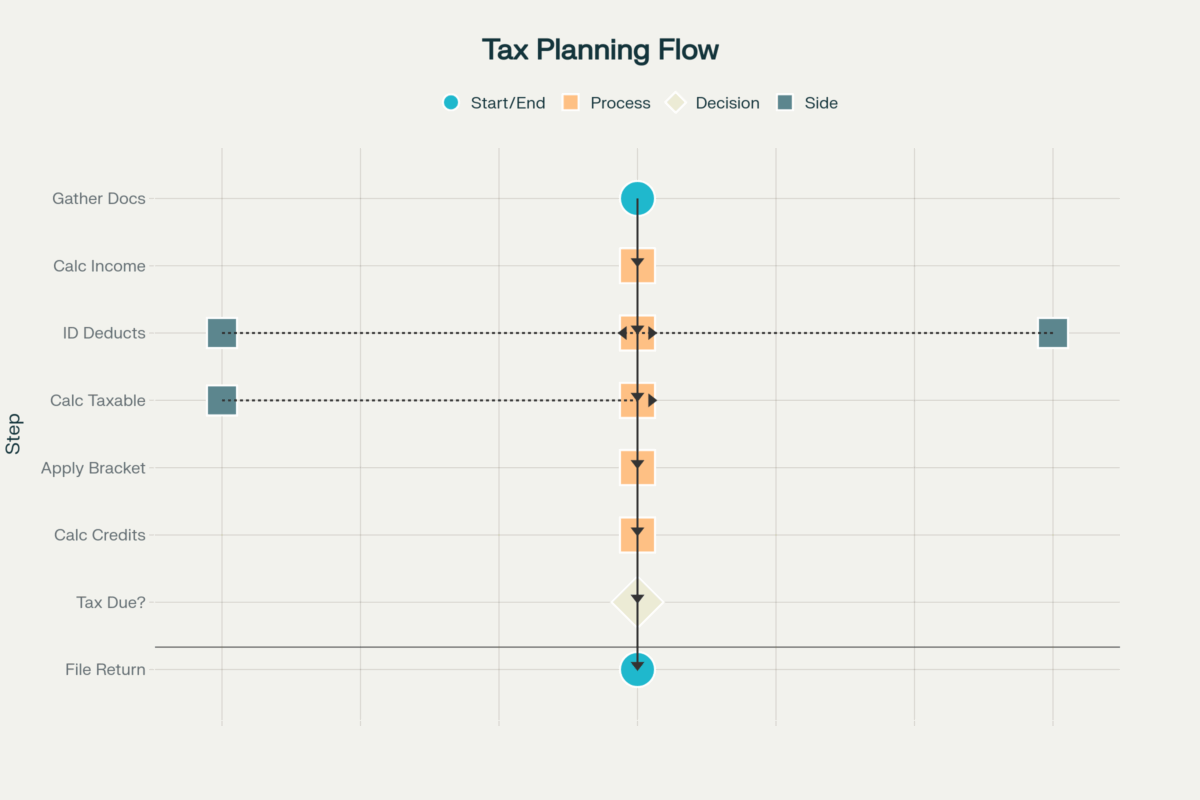

Essential Tax Planning Process

Following a systematic approach ensures you don’t miss any opportunities to save:

Step-by-step tax planning flowchart for Canadian taxpayers

Step-by-Step Tax Planning

- Gather Documents: Collect all T4s, T5s, receipts, and investment statements

- Calculate Total Income: Add employment, investment, and other income

- Identify Deductions: RRSP contributions, moving expenses, child care costs

- Calculate Taxable Income: Total income minus deductions

- Apply Tax Brackets: Use federal and provincial rates

- Calculate Credits: Basic personal amount, medical, charitable donations

- Determine Refund/Owing: Compare calculated tax to amounts already paid

- File Return: Submit by deadline to avoid penalties

Important Dates for 2025

Mark these crucial deadlines in your calendar:

| Date | Deadline | Who It Affects |

|---|---|---|

| February 24, 2025 | Earliest online filing date | All taxpayers |

| March 3, 2025 | RRSP contribution deadline | RRSP contributors |

| April 30, 2025 | Tax filing deadline | Most individuals |

| April 30, 2025 | Tax payment deadline | Anyone owing taxes |

| June 15, 2025 | Self-employed filing deadline | Self-employed individuals |

| July 1, 2025 | Middle-class tax cut effective | All taxpayers |

Tax Planning Checklist for 2025

Before Tax Season

- Update personal information with CRA (address, direct deposit, marital status)

- Gather all tax documents (T4, T5, receipts, investment statements)

- Make final RRSP contributions by March 3, 2025

- Organize receipts for medical expenses, charitable donations, home office

- Review investment portfolio for tax-loss harvesting opportunities

During Tax Season

- File early (starting February 24) to get refund faster

- Claim all eligible deductions and credits

- Double-check calculations before submitting

- Keep copies of all documents and returns

- Pay any taxes owing by April 30 to avoid penalties

After Filing

- Review Notice of Assessment for errors or missed opportunities

- Update contribution room for RRSP and TFSA

- Plan next year’s strategy based on this year’s results

- Set up automatic savings for RRSP and TFSA contributions

Maximizing Your Tax Savings: Advanced Strategies

Income Splitting Opportunities

- Pension income splitting: Share up to 50% of eligible pension income with spouse

- Spousal RRSP: Higher-earning spouse contributes to lower-earning spouse’s RRSP

- Family business: Pay reasonable salaries to family members

Investment Tax Strategies

- Tax-loss harvesting: Sell losing investments to offset capital gains

- Asset location: Hold interest-bearing investments in tax-sheltered accounts

- Dividend tax credit: Take advantage of preferential dividend tax treatment

Business and Self-Employment

- Home office deduction: Claim percentage of home expenses

- Business expenses: Deduct legitimate business costs

- Professional development: Training costs are often deductible

Common Tax Mistakes to Avoid

Missing Deductions

- Forgetting RRSP room: Check your Notice of Assessment for available room

- Overlooking medical expenses: Include all family members’ expenses

- Missing employment expenses: Tools, union dues, professional fees

Filing Errors

- Late filing penalties: File by deadline even if you can’t pay

- Incorrect information: Double-check all numbers and personal details

- Missing signatures: Both spouses must sign if filing jointly

Planning Mistakes

- Waiting until last minute: Start planning early in the year

- Ignoring carry-forwards: Use unused credits from previous years

- Not keeping records: Maintain organized tax records for at least 6 years

Sample Tax Calculations by Income Level

Here’s how the new tax brackets affect different income levels for Ontario residents:

| Income Level | Federal Tax | Provincial Tax | Total Tax | After-Tax Income | Average Tax Rate |

|---|---|---|---|---|---|

| $40,000 | $3,800 | $1,319 | $5,119 | $34,881 | 12.8% |

| $60,000 | $6,188 | $2,545 | $8,733 | $51,267 | 14.6% |

| $80,000 | $9,688 | $4,070 | $13,758 | $66,242 | 17.2% |

| $100,000 | $13,188 | $5,595 | $18,783 | $81,217 | 18.8% |

| $150,000 | $22,188 | $9,595 | $31,783 | $118,217 | 21.2% |

*Note: Estimates exclude CPP/EI premiums and other deductions

Getting Help When You Need It

Free Resources

- CRA website: canada.ca for official information and forms

- Volunteer tax clinics: Free tax preparation for low-income individuals

- CRA phone line: 1-800-959-8281 for general inquiries

Professional Help

- Certified tax preparers: For complex situations

- Accountants: For business owners and high-net-worth individuals

- Financial advisors: For comprehensive tax and investment planning

Looking Ahead: Planning for 2026

Confirmed Changes

- Lowest tax bracket drops to 14% (from 14.5% in 2025)

- Additional tax savings of approximately $140 per person

- Continued indexation of tax brackets to inflation

Planning Opportunities

- Maximize 2025 savings: Take advantage of current rates

- Plan RRSP strategy: Consider multi-year contribution planning

- Review investment allocation: Optimize for tax efficiency

Conclusion: Take Action Now

Canada’s 2025 tax changes represent a significant opportunity to save money, but only if you take action. The new middle-class tax cut, combined with smart tax planning strategies, can put hundreds or even thousands of dollars back in your pocket.

Your next steps:

- Calculate your potential savings using the new tax brackets

- Maximize your RRSP contributions by the March 3 deadline

- Organize your tax documents and file early

- Review your overall tax strategy for 2025 and beyond

Remember, tax planning isn’t a once-a-year activity – it’s an ongoing process that can significantly impact your financial health. Start implementing these strategies today, and you’ll be well on your way to minimizing your tax burden and maximizing your savings.

Need more personalized advice? Consider consulting with a qualified tax professional who can help you navigate the complexities of the Canadian tax system and develop a strategy tailored to your specific situation.

This guide is for informational purposes only and should not be considered professional tax advice. Tax laws are complex and can change. Always consult with a qualified tax professional for advice specific to your situation.