CPP & OAS Increases 2025: Find Out Your New Payments

Canadian seniors, it’s time to celebrate! The 2025 updates to the Canada Pension Plan (CPP) and Old Age Security (OAS) bring meaningful increases to your monthly payments, ensuring your retirement income keeps pace with the rising cost of living. Whether you’re already receiving benefits or preparing to apply, this comprehensive guide will walk you through everything you need to know about the 2025 changes, payment amounts, and how to access your benefits.

Canadian seniors, it’s time to celebrate! The 2025 updates to the Canada Pension Plan (CPP) and Old Age Security (OAS) bring meaningful increases to your monthly payments, ensuring your retirement income keeps pace with the rising cost of living.

Whether you’re already receiving benefits or preparing to apply, this comprehensive guide will walk you through everything you need to know about the 2025 changes, payment amounts, and how to access your benefits.

Understanding Your Canadian Pension Benefits

Before diving into the 2025 increases, let’s clarify what CPP and OAS actually are and how they work together to support your retirement.

What is CPP (Canada Pension Plan)?

The Canada Pension Plan is a contributory pension program that you pay into throughout your working years. Think of it as a government-backed retirement savings plan where:

- You contribute 5.95% of your earnings (matched by your employer)

- Your contributions are based on earnings between $3,500 and $71,300 in 2025

- You can start receiving payments as early as age 60 (with reductions) or delay until age 70 (with increases)

What is OAS (Old Age Security)?

Old Age Security is a non-contributory pension funded by general tax revenue. This means:

- You don’t pay into it during your working years

- It’s available to most Canadian residents aged 65 and older

- You need to have lived in Canada for at least 10 years after age 18

- Higher-income earners may face a “clawback” if their income exceeds $90,997

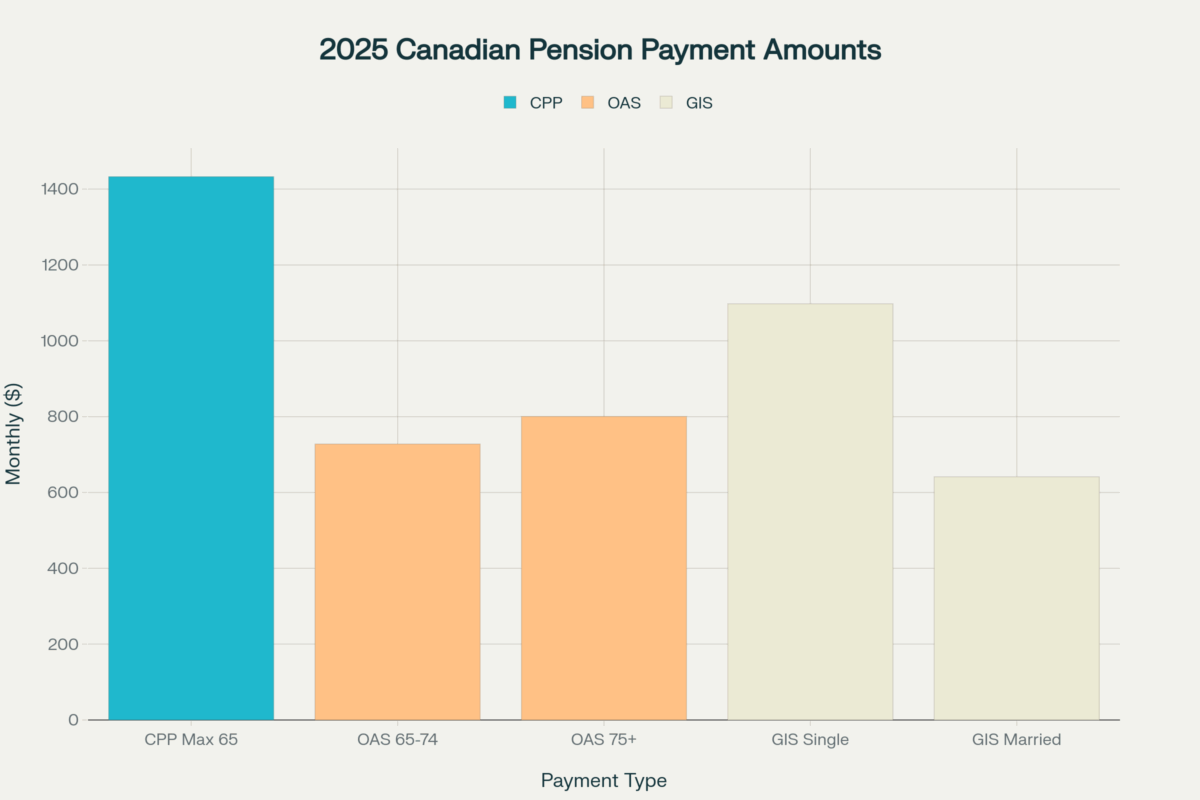

2025 Payment Amounts: What You Can Expect

The good news is that both CPP and OAS payments are increasing in 2025, thanks to inflation adjustments and the ongoing CPP enhancement program.

CPP Payment Amounts for 2025

- Maximum monthly payment: $1,433 (at age 65)

- Maximum annual payment: $17,197 (at age 65)

- Average monthly payment: Approximately $832 (up from $772 in 2024)

OAS Payment Amounts for 2025

GIS (Guaranteed Income Supplement) 2025

For low-income seniors receiving OAS:

2025 Canadian Pension Payment Amounts – Monthly maximums for CPP, OAS, and GIS benefits

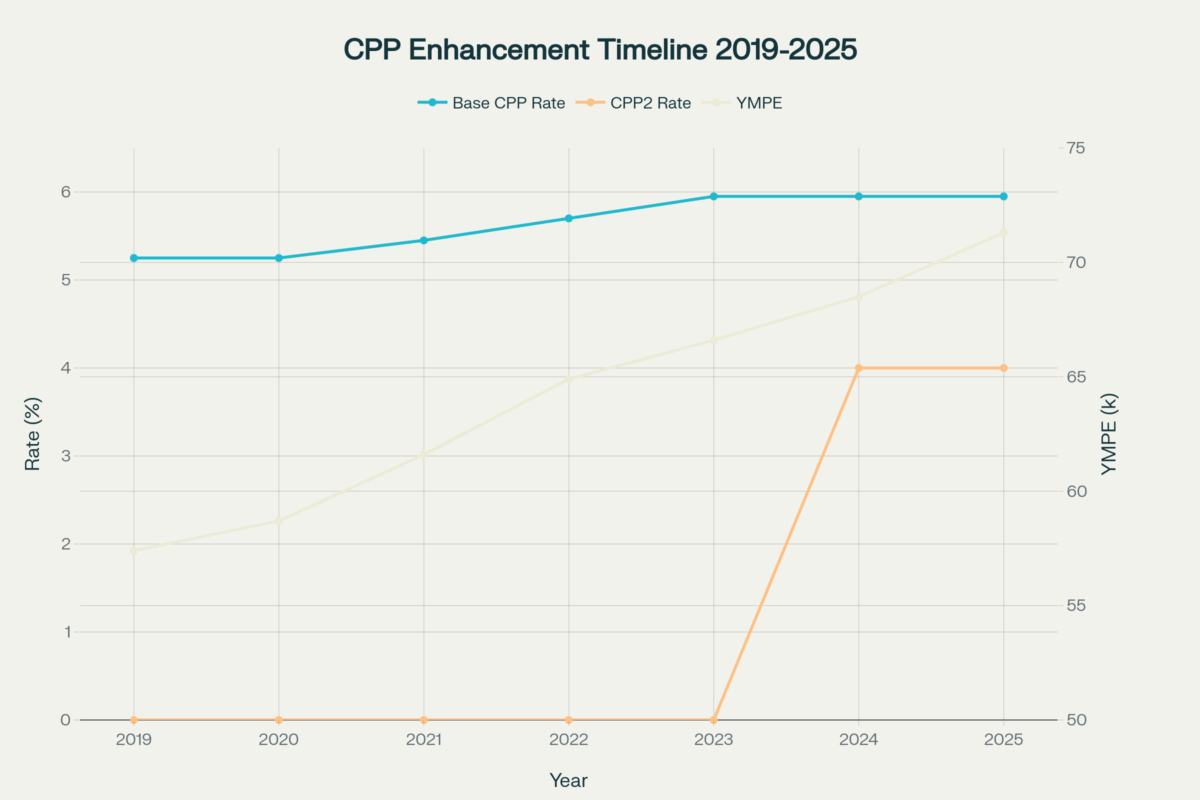

CPP Enhancement Program: Building Better Benefits

The CPP enhancement program, which began in 2019 and reaches full implementation in 2025, is designed to increase your retirement income from 25% to 33.33% of your average working income.

Phase 1 (2019-2023): Contribution Rate Increases

The first phase gradually increased contribution rates from 4.95% to 5.95% for both employees and employers:

- 2019: 5.25%

- 2020: 5.25%

- 2021: 5.45%

- 2022: 5.70%

- 2023: 5.95%

Phase 2 (2024-2025): Higher Earning Limits

The second phase introduces CPP2 – additional contributions on higher earnings:

- 2024: CPP2 contributions of 4% on earnings between $68,500 and $73,200

- 2025: CPP2 contributions of 4% on earnings between $71,300 and $81,200

CPP Enhancement Timeline 2019-2025 – Shows the progression of contribution rates and maximum pensionable earnings

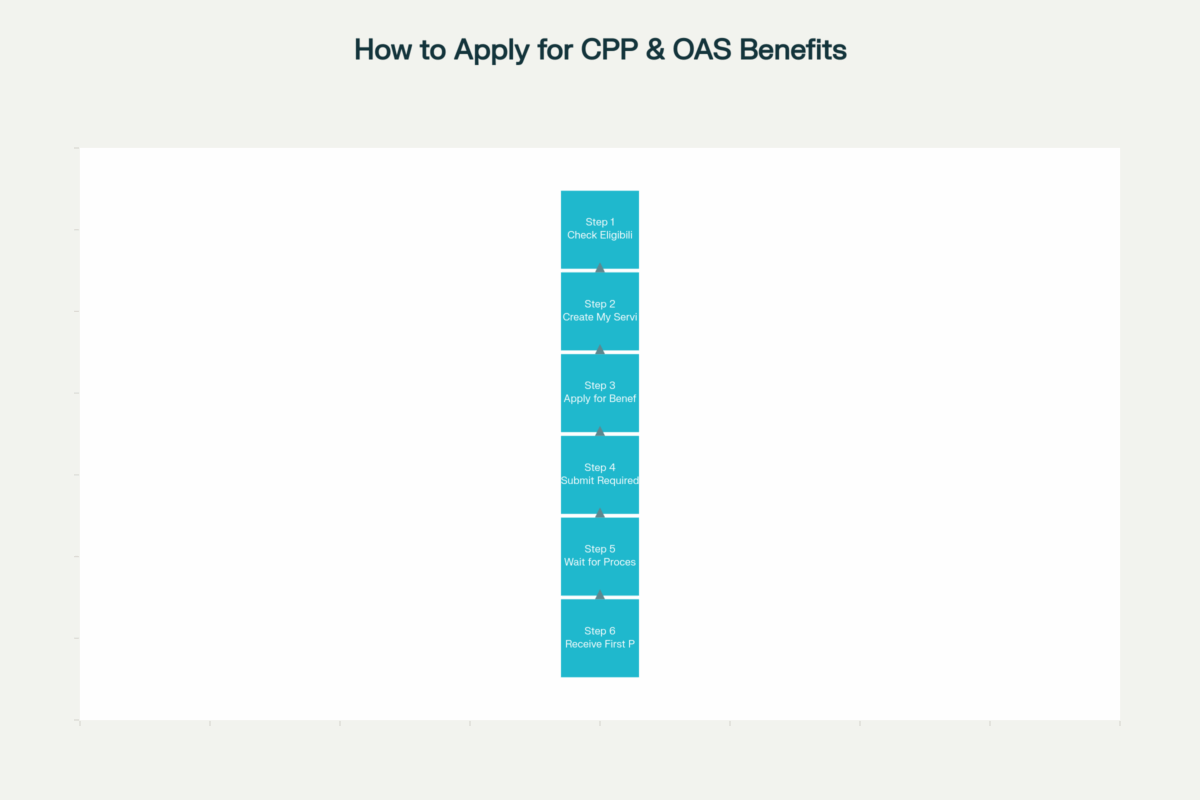

How to Apply for CPP and OAS Benefits

Applying for your pension benefits doesn’t have to be complicated. Here’s your step-by-step guide to getting started.

Step 1: Check Your Eligibility

CPP Eligibility:

- Age 60 or older (with reductions if taken before 65)

- At least one valid contribution to CPP during your working years

- Legal residence in Canada for at least 10 years

OAS Eligibility:

- Age 65 or older

- Canadian citizen or legal resident

- Lived in Canada for at least 10 years after age 18

- 20 years in Canada if you currently live outside the country

Step 2: Create Your My Service Canada Account

Your My Service Canada Account is your gateway to applying for and managing your benefits:

- Visit canada.ca/my-service-canada-account

- Choose your registration method:

- GCKey (government username and password)

- Banking partner (use your online banking credentials)

- Provincial digital ID (available in some provinces)

- Complete identity verification

- Set up security questions and recovery options

Step 3: Submit Your Applications

CPP Application:

- Apply up to 12 months before your desired start date

- Choose your starting age (60-70) and understand payment adjustments

- Complete the online application through My Service Canada Account

OAS Application:

- Apply 11 months before turning 65 (if not automatically enrolled)

- Most eligible seniors receive automatic enrollment letters

- Include GIS application if you have low income

How to Apply for CPP & OAS Benefits – Step-by-step application process flowchart

Essential Application Checklist

To ensure a smooth application process, use this comprehensive checklist to prepare:

Before You Apply

□ Check if you meet eligibility requirements (age and residency)

□ Gather required documents (birth certificate, citizenship/immigration papers)

□ Ensure you have a Social Insurance Number (SIN)

□ Collect banking information for direct deposit setup

□ Calculate your expected benefit amounts using online calculators

Setting Up Your Account

□ Visit canada.ca/my-service-canada-account

□ Choose registration method (GCKey, banking partner, or provincial ID)

□ Complete identity verification process

□ Set up security questions and recovery options

□ Test your account login and explore the dashboard

CPP Application Steps

□ Apply up to 12 months before your desired start date

□ Decide on your starting age (60-70) and understand payment adjustments

□ Complete the online application through My Service Canada Account

□ Upload required supporting documents

□ Review and submit your application

□ Note your confirmation number and save application receipt

OAS Application Steps

□ Apply 11 months before turning 65 (if not automatically enrolled)

□ Check if you received an automatic enrollment letter

□ Complete the OAS application online or by mail

□ Include GIS application if you have low income

□ Provide proof of residency in Canada

□ Submit citizenship or immigration documents if born outside Canada

After Applying

□ Monitor your application status online

□ Respond promptly to any Service Canada requests for additional information

□ Set up direct deposit if not already configured

□ Review your first payment statement carefully

□ Keep records of all correspondence and payment information

□ Set up tax withholding if desired

Annual Maintenance

□ File your income tax return on time (affects GIS eligibility)

□ Report any changes in marital status, address, or banking information

□ Review annual adjustment letters for payment changes

□ Update your My Service Canada Account information regularly

□ Keep your contact information current with Service Canada

2025 Payment Schedule

Both CPP and OAS payments are made on the same dates each month, typically the third-to-last business day. Here are the exact payment dates for 2025:

| Month | Payment Date |

|---|---|

| January | January 29, 2025 |

| February | February 26, 2025 |

| March | March 27, 2025 |

| April | April 28, 2025 |

| May | May 28, 2025 |

| June | June 26, 2025 |

| July | July 29, 2025 |

| August | August 27, 2025 |

| September | September 25, 2025 |

| October | October 29, 2025 |

| November | November 26, 2025 |

| December | December 22, 2025 |

Important Notes:

- Direct deposit recipients receive funds on these exact dates

- Mail recipients should allow 5-10 business days for delivery

- Set up direct deposit for faster, more reliable payments

Understanding Your Payment Adjustments

Both CPP and OAS payments are adjusted regularly to keep pace with inflation and ensure your purchasing power is maintained.

CPP Inflation Adjustments

CPP payments are adjusted annually based on the Consumer Price Index (CPI). For 2025, CPP payments increased by 2.7% based on the inflation rate from October 2024.

OAS Inflation Adjustments

OAS payments are reviewed quarterly (January, April, July, October) and adjusted based on CPI changes. For July 2025, OAS benefits increased by 1.0% for the quarter, representing a 2.3% annual increase.

Maximizing Your Benefits: Pro Tips

Timing Your CPP Application

- Age 60: 36% reduction from full pension (0.6% per month)

- Age 65: Full pension amount

- Age 70: 42% increase from full pension (0.7% per month)

OAS Deferral Strategy

You can defer OAS for up to 5 years (until age 70) and receive a 0.6% increase per month, up to a maximum 36% increase.

Income Management for OAS

To avoid the OAS clawback:

- Keep your net income below $90,997 (2024 threshold)

- Consider pension income splitting with your spouse

- Review your RRIF withdrawal strategy

CPP vs OAS: Key Differences at a Glance

Understanding the differences between CPP and OAS helps you plan your retirement income strategy:

| Feature | CPP | OAS |

|---|---|---|

| Benefit Type | Contributory pension | Non-contributory pension |

| Eligibility Age | 60+ (reduced) / 65 (full) / 70 (maximum) | 65+ |

| Contribution Required | Yes – based on employment earnings | No – funded by general tax revenue |

| Maximum Monthly (2025) | $1,433 (at age 65) | $727.67 (65-74) / $800.44 (75+) |

| Income Testing | No income testing | Yes – clawback above $90,997 |

| Automatic Enrollment | No – must apply | Most eligible seniors |

| Enhancement Program | Yes – ongoing until 2025 | No enhancement program |

Common Questions and Answers

Q: Can I receive both CPP and OAS?

u003cstrongu003eA:u003c/strongu003e Yes! Most Canadian retirees receive both benefits, as they serve different purposes and have different eligibility requirementsu003ca href=u0022https://www.planeasy.ca/the-cpp-max-will-be-huge-in-the-future/u0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003eu003ca href=u0022https://www.pspp.ca/members/your-pension/how-are-your-contributions-calculated/u0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e.

Q: What happens if I work while receiving CPP or OAS?

u003cstrongu003eA:u003c/strongu003e You can continue working while receiving both benefits. CPP won’t be reduced, and you may qualify for u003cstrongu003ePost-Retirement Benefitsu003c/strongu003eu003ca href=u0022https://delhitechnicalcampus.com/canada-pension-2025-overhaul/u0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e. OAS may be affected by the income clawback if your total income exceeds the thresholdu003ca href=u0022https://www.pspp.ca/members/your-pension/how-are-your-contributions-calculated/u0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e.

Q: How do I know if I’m automatically enrolled for OAS?

u003cstrongu003eA:u003c/strongu003e Service Canada tries to automatically enroll eligible seniors. You’ll receive a letter by your 64th birthday if you qualifyu003ca href=u0022https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/canada-pension-plan-cpp/cpp-contribution-rates-maximums-exemptions.htmlu0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003eu003ca href=u0022https://www.mun.ca/hr/media/production/memorial/administrative/human-resources/media-library/services/Enhancement-to-the-Canada-Pension-Plan-Program-2025update.pdfu0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e. If you don’t receive a letter, you need to apply manuallyu003ca href=u0022https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/canada-pension-plan-cpp/cpp-contribution-rates-maximums-exemptions.htmlu0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003eu003ca href=u0022https://www.mun.ca/hr/media/production/memorial/administrative/human-resources/media-library/services/Enhancement-to-the-Canada-Pension-Plan-Program-2025update.pdfu0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e.

Q: Can I change my CPP start date after applying?

u003cstrongu003eA:u003c/strongu003e You can cancel your CPP application and reapply with a different start date, but only within specific timeframes and conditionsu003ca href=u0022https://delhitechnicalcampus.com/canada-pension-2025-overhaul/u0022 target=u0022_blanku0022 rel=u0022noreferrer noopeneru0022u003eu003c/au003e. Contact Service Canada for specific guidance.

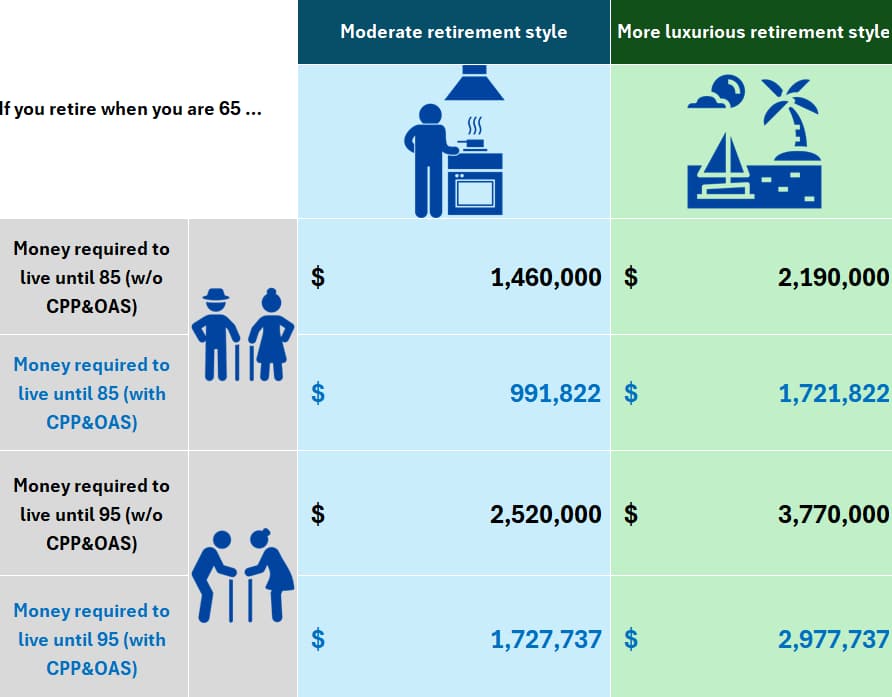

The Impact on Your Retirement Planning

Understanding how CPP and OAS fit into your overall retirement income is crucial for financial planning.

Estimated retirement savings needed in Canada with and without CPP and OAS benefits for moderate and luxurious retirement styles

The enhanced CPP benefits will be particularly valuable for younger workers who contribute to the enhanced program for their entire careers. For someone earning $50,000 annually throughout their working life, the enhanced CPP could provide approximately $16,000 per year instead of the current $12,000.

Getting Help and Support

Don’t hesitate to seek assistance if you need help with your applications or have questions about your benefits.

Service Canada Resources

- Online: canada.ca/my-service-canada-account

- Phone: 1-800-277-9914 (CPP) or 1-800-277-9915 (OAS)

- TTY: 1-800-255-4786

- In-person: Visit your local Service Canada office

What to Bring to Service Canada

- Social Insurance Number

- Birth certificate

- Citizenship or immigration documents

- Banking information for direct deposit

- Marriage certificate (if applicable)

Your Next Steps

Now that you understand the 2025 CPP and OAS increases, here’s what you should do:

- Calculate your estimated benefits using the online calculators at canada.ca

- Create your My Service Canada Account if you haven’t already

- Apply for benefits at the appropriate times (CPP: up to 12 months before, OAS: 11 months before turning 65)

- Set up direct deposit for faster, more reliable payments

- Keep your information updated with Service Canada

- File your taxes on time to maintain GIS eligibility

- Review your payments annually and report any changes

Conclusion

The 2025 increases to CPP and OAS represent a significant step forward in supporting Canadian seniors’ financial security. With maximum CPP payments reaching $1,433 per month and OAS payments adjusted for inflation, these benefits provide a stronger foundation for your retirement income.

Remember that these programs are designed to work together with your personal savings and employer pensions to provide comprehensive retirement security. By understanding the application process, payment schedules, and optimization strategies outlined in this guide, you’ll be well-equipped to maximize your benefits and enjoy a more secure retirement.

The key to success is starting early and staying informed. Whether you’re approaching retirement or already receiving benefits, regularly reviewing your situation and keeping up with program changes will help ensure you receive all the benefits you’re entitled to.

Take action today by creating your My Service Canada Account and beginning the application process. Your future self will thank you for taking these important steps toward a more secure retirement.