Capital Gains Tax 2025: Canada’s Latest Changes

If you’ve been worried about Canada’s proposed capital gains tax increases, here’s some good news: the controversial changes have been cancelled. Prime Minister Mark Carney announced in March 2025 that the government would not proceed with the planned increase to the capital gains inclusion rate. This means the capital gains tax system remains much more favorable for Canadian taxpayers than initially feared.

This comprehensive guide will walk you through everything you need to know about capital gains tax in Canada for 2025, from basic concepts to advanced planning strategies. Whether you’re selling stocks, real estate, or running a small business, understanding these rules can save you thousands of dollars.

What Are Capital Gains and How Are They Taxed?

Capital gains occur when you sell an asset (like stocks, real estate, or business shares) for more than you paid for it. In Canada, capital gains receive preferential tax treatment compared to regular income like your salary.

Here’s how it works:

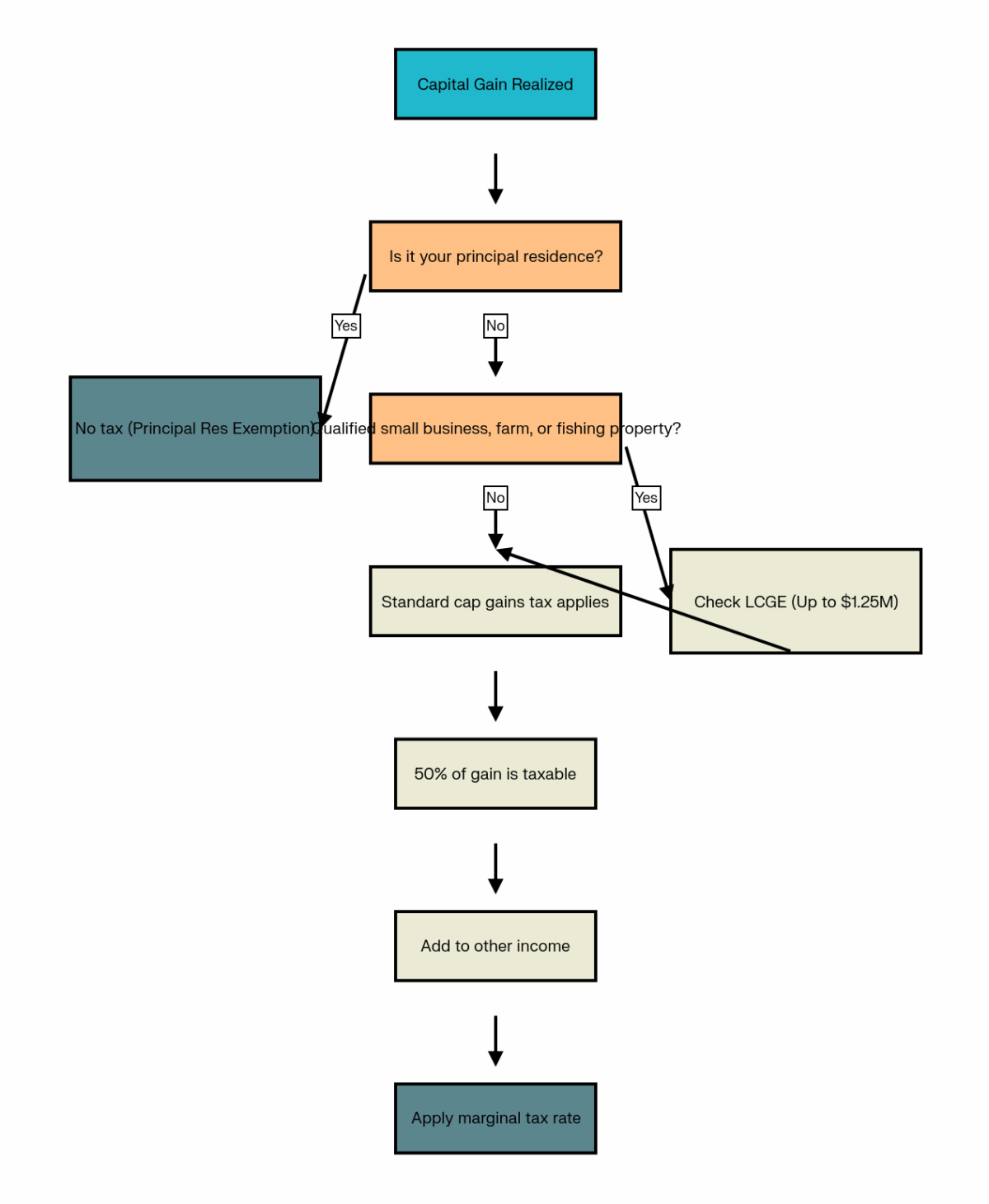

- Only 50% of your capital gain is taxable (called the “inclusion rate”)

- This taxable portion is added to your other income

- You pay tax at your marginal tax rate on this amount

- The other 50% is completely tax-free

Canada Capital Gains Tax 2025: Key Facts at a Glance – Essential information for taxpayers

Simple Example

If you buy stocks for $10,000 and sell them for $15,000:

- Capital gain = $5,000

- Taxable amount = $2,500 (50% of $5,000)

- Tax owed = $2,500 × your marginal tax rate

Capital Gains Tax Decision Flow Chart – A simple guide to determine your tax liability on capital gains in Canada

Current Status: What Changed in 2025?

The Proposed Increase is Cancelled

The federal government had originally proposed increasing the capital gains inclusion rate from 50% to 66.67% for:

- Individuals with annual capital gains over $250,000

- All gains realized by corporations and trusts

However, this proposal faced significant opposition and has been officially cancelled. The inclusion rate remains at 50% for all individual taxpayers, regardless of the amount of their capital gains.

What Actually Changed

The only change that took effect is the Lifetime Capital Gains Exemption (LCGE) increase:

- Old limit: $1,016,836

- New limit: $1.25 million (effective June 25, 2024)

- This applies to qualifying small business corporation shares and farm/fishing property

Understanding Capital Gains Tax Rates Across Canada

Since capital gains are taxed as regular income, your rate depends on your total income and province of residence. Here are the effective capital gains tax rates (including provincial taxes) for 2025:

| Income Level | Ontario | British Columbia | Alberta | Quebec |

|---|---|---|---|---|

| Up to $57,375 | 10.02% | 10.03% | 12.50% | 14.50% |

| $57,376 – $114,750 | 14.82% | 14.10% | 15.25% | 19.75% |

| $114,751 – $177,882 | 18.58% | 19.14% | 18.00% | 25.00% |

| $177,883 – $253,414 | 20.58% | 22.01% | 20.66% | 27.38% |

| Over $253,414 | 23.08% | 26.75% | 23.50% | 29.38% |

Note: These rates represent 50% of the combined federal and provincial marginal tax rates.

Major Exemptions You Need to Know

1. Principal Residence Exemption

Your home is completely tax-free when you sell it, provided it was your principal residence. This is one of Canada’s most valuable tax benefits.

Key requirements:

- You or your family must have “ordinarily inhabited” the property

- You can only designate one property per family as your principal residence each year

- Cottages and vacation homes can qualify if they meet the criteria

- You must report the sale on Schedule 3 and Form T2091, even though no tax is owed

Canada Revenue Agency Schedule 3 form section for reporting the sale of a principal residence and claiming the principal residence exemption on capital gains tax

2. Lifetime Capital Gains Exemption (LCGE)

For 2025, you can shelter up to $1.25 million in capital gains from tax when selling:

- Qualifying small business corporation (QSBC) shares

- Qualifying farm property

- Qualifying fishing property

Requirements for QSBC shares:

- Must be shares of a Canadian-controlled private corporation

- At least 90% of assets must be used in active business in Canada

- You must have owned the shares for at least 24 months

3. Tax-Sheltered Accounts

Investments held in these accounts are completely exempt from capital gains tax:

- Tax-Free Savings Account (TFSA): $7,000 contribution limit for 2025

- Registered Retirement Savings Plan (RRSP): $32,490 limit for 2025

- Registered Education Savings Plan (RESP)

- First Home Savings Account (FHSA)

Types of Investments and Capital Gains Tax

Stocks and Securities

When you sell stocks, bonds, ETFs, or mutual funds outside registered accounts, you’ll owe capital gains tax on any profit. This includes:

- Individual stocks on Canadian and foreign exchanges

- Mutual funds and ETF units

- Corporate and government bonds

- Options and derivatives

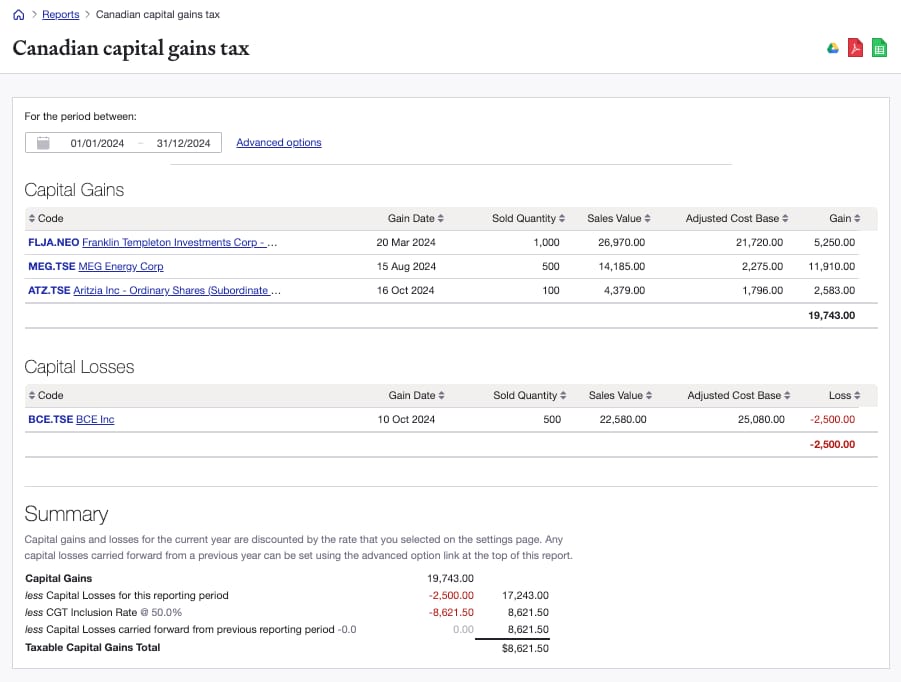

Canadian capital gains tax report showing detailed gains, losses, and taxable capital gains summary for 2024

Real Estate Investment Property

Investment properties (not your principal residence) are subject to capital gains tax. This includes:

- Rental properties

- Vacant land

- Commercial real estate

- Foreign real estate

Special consideration: If you flip properties (buy and sell within 12 months), the CRA may treat the entire gain as business income (100% taxable) rather than capital gains.

Cryptocurrency

The Canada Revenue Agency treats cryptocurrency as property, subject to capital gains tax. Tax applies when you:

- Sell crypto for Canadian dollars

- Trade one cryptocurrency for another

- Use crypto to purchase goods or services

- Gift cryptocurrency to someone

Key point: Only 50% of crypto gains are taxable for individual investors, but if the CRA determines you’re running a crypto business, 100% of gains become taxable as business income.

Small Business Sales

Selling your business can result in significant capital gains, but the LCGE provides substantial protection. With the 2025 increase to $1.25 million, most small business owners can sell their company tax-free if it qualifies as a QSBC.

Smart Tax Planning Strategies

1. Tax-Loss Harvesting

This strategy involves selling investments at a loss to offset capital gains. Key rules:

- Capital losses can offset capital gains dollar-for-dollar

- Losses can be carried back 3 years or forward indefinitely

- Superficial loss rule: You cannot buy back the same investment within 30 days before or after selling

2. Timing Your Sales

Consider the timing of asset sales to optimize your tax situation:

- Spread large gains across multiple years to stay in lower tax brackets

- Harvest losses in high-income years to offset gains

- Realize gains in low-income years (like early retirement)

3. Income Splitting Strategies

Legal ways to split capital gains with family members:

- Spousal transfers: Transfer assets to spouse in a lower tax bracket

- Attribution rules: Be aware that income attribution may apply

- Joint ownership: Consider joint ownership of investment properties

4. Maximize Registered Accounts

Prioritize investing in tax-sheltered accounts:

- Use your full TFSA contribution room ($7,000 for 2025)

- Maximize RRSP contributions (deadline: March 1, 2025)

- Consider spousal RRSPs for income splitting in retirement

Filing Requirements and Key Deadlines

Important Dates for 2025

Key Capital Gains Tax Dates and Deadlines for 2025 – Important dates for tax planning and compliance

Critical deadlines:

- March 1, 2025: RRSP contribution deadline for 2024 tax year

- April 30, 2025: Income tax return filing deadline for most individuals

- June 2, 2025: Extended deadline with penalty relief for capital gains filers

- June 15, 2025: Filing deadline for self-employed individuals

Required Forms

When you have capital gains or losses, you must file:

Schedule 3: Capital Gains (or Losses)

- Required for all capital gains and losses

- Separate sections for different types of property

- Must be filed even if no tax is owed

Canada Revenue Agency Schedule 3 form for reporting capital gains or losses, showing sections for different types of assets and calculation fields

Form T2091: Principal Residence Designation

- Required when selling your principal residence

- Must be filed even though no tax is typically owed

- Calculates the principal residence exemption

Form T1135: Foreign Income Verification Statement

- Required if you own foreign property worth more than $100,000

- Includes foreign stocks, bonds, and real estate

Common Mistakes to Avoid

Record-Keeping Errors

- Not tracking adjusted cost base (ACB) properly

- Missing transaction fees and commissions in calculations

- Poor documentation of purchase and sale dates

- Losing receipts for capital improvements

Timing Mistakes

- Triggering superficial losses by repurchasing within 30 days

- Not planning year-end tax-loss harvesting

- Missing filing deadlines and incurring penalties

- Forgetting about attribution rules on spousal transfers

Reporting Errors

- Not reporting principal residence sales (even though tax-free)

- Incorrectly calculating inclusion rates

- Missing foreign property reporting requirements

- Confusing capital gains with business income

Your 2025 Capital Gains Tax Checklist

Here’s your comprehensive action plan for managing capital gains tax in 2025:

Record Keeping (Ongoing)

🔴 High Priority:

- Track all investment purchases with dates and amounts

- Keep records of all investment sales and disposals

- Gather all T3, T5, and investment slips

- Calculate adjusted cost base (ACB) for all investments

🟡 Medium Priority:

- Document all reinvested dividends and distributions

- Maintain records of transaction fees and costs

Tax Planning (Before December 31)

🔴 High Priority:

- Review capital gains and losses before year-end

- Consider tax-loss harvesting opportunities

- Maximize TFSA and RRSP contributions (deadline: March 1)

🟡 Medium Priority:

- Plan timing of asset sales for tax efficiency

- Evaluate principal residence exemption eligibility

Filing & Reporting (By April 30)

🔴 High Priority:

- Complete Schedule 3 for all capital gains/losses

- File Form T2091 for principal residence sales

- File tax return by April 30 (or June 15 if self-employed)

- Pay any taxes owed to avoid interest charges

🟡 Medium Priority:

- Report foreign property on Form T1135 (if applicable)

Compliance & Ongoing

🔴 High Priority:

- File tax return by deadline to avoid penalties

- Pay taxes owed on time

🟡 Medium Priority:

- Keep all supporting documents for 6 years

- Consider professional tax advice for complex situations

Real-World Examples: What You’ll Actually Pay

Here are practical examples showing how capital gains tax works for different scenarios in Ontario:

| Investment Type | Capital Gain | Taxable Amount | Approximate Tax |

|---|---|---|---|

| Stocks (low income) | $3,000 | $1,500 | $301 |

| Real Estate | $200,000 | $100,000 | $29,650 |

| Small Business | $1,500,000 | $0 (LCGE applies) | $0 |

| Cryptocurrency | $7,000 | $3,500 | $1,038 |

| Cottage | $200,000 | $100,000 | $37,160 |

These examples assume Ontario tax rates and varying income levels

Looking Ahead: What to Expect

Policy Stability

With the cancellation of the proposed capital gains tax increase, the current system appears stable for the foreseeable future. The 50% inclusion rate has been in place since 2001 and is likely to remain unchanged.

Focus on Planning

Given the policy certainty, focus on:

- Maximizing exemptions (principal residence, LCGE, registered accounts)

- Strategic timing of asset sales

- Proper record-keeping for all investments

- Regular portfolio review for tax optimization opportunities

Conclusion

Canada’s capital gains tax system for 2025 is more taxpayer-friendly than many initially feared. With the proposed increase cancelled and the LCGE raised to $1.25 million, most Canadians can effectively manage their capital gains tax burden through proper planning.

Key takeaways:

- 50% inclusion rate remains unchanged for all individual taxpayers

- Principal residence sales remain completely tax-free

- LCGE increased to $1.25 million for qualifying properties

- Proper planning can significantly reduce your tax burden

- Good record-keeping is essential for compliance and optimization

Remember, tax laws can be complex, and everyone’s situation is different. For significant transactions or complex situations, consider consulting with a qualified tax professional who can provide personalized advice based on your specific circumstances.

By following this guide and staying organized with your record-keeping and planning, you’ll be well-positioned to minimize your capital gains tax burden while staying fully compliant with Canadian tax law.